The 50-30-20 Rule: What it is and how to apply it to organize your finances

If you have ever wondered “where does your money go,” then the 50/30/20 rule may be the simplest way to organize your personal finances and start saving without complications. Summary: The 50-30-20 rule suggests dividing your income into 50% for needs, 30% for wants, and 20% for savings in order to maintain a sustainable financial […]

If you have ever wondered “where does your money go,” then the 50/30/20 rule may be the simplest way to organize your personal finances and start saving without complications.

Summary: The 50-30-20 rule suggests dividing your income into 50% for needs, 30% for wants, and 20% for savings in order to maintain a sustainable financial balance.

In this guide, you will learn exactly what it is, how to apply it step by step, and how to adapt it to your actual situation.

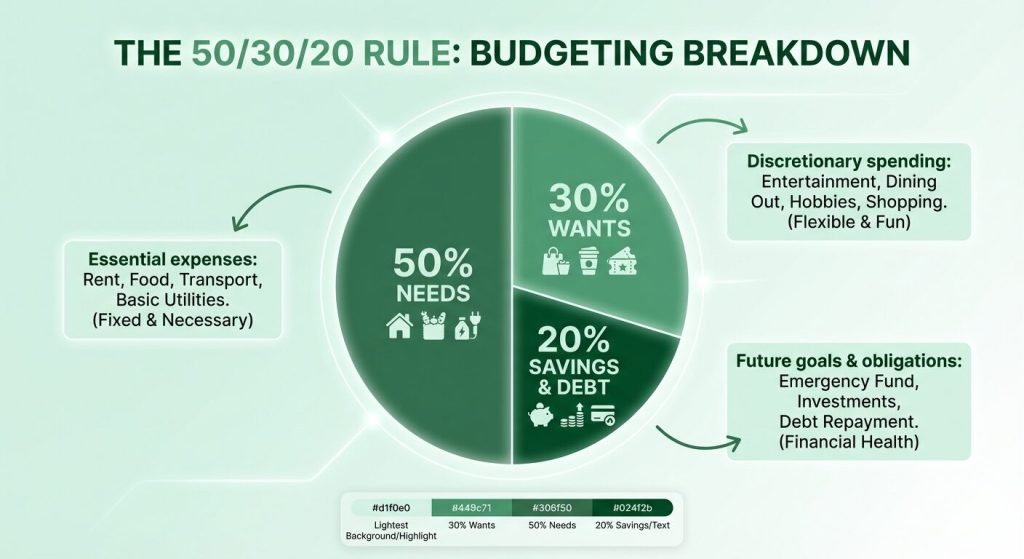

What is the 50-30-20 Rule and why does it work?

Essentially, the 50-30-20 rule is a budgeting method that divides your monthly income into three clear categories:

- 50% for necessities (essential expenses that you cannot avoid)

- 30% for desires (likes and entertainment)

- 20% for savings (or debt repayment)

It was popularized by Elizabeth Warren (US senator and bankruptcy expert) in her book “All Your Worth.” Its simplicity is what makes it so effective: you don’t need complicated spreadsheets or advanced financial knowledge.

How the 50-30-20 Rule works with a real-life example

For example, suppose you earn R$500,000 per month. In this case, the amount would be distributed as follows:

| Category | Percentage | Value |

|---|---|---|

| Requirements | 50% | $250,000 |

| Desires | 30% | $150,000 |

| Economy | 20% | $100,000 |

50% for Necessities

First, there are the expenses you have to pay to live:

- Rent or mortgage

- Utilities (electricity, water, gas, internet)

- Supermarket and basic food items

- Transportation to work

- Health (medical care, essential medicines)

- Minimum mandatory debts

Key: If your needs exceed 50%, this is clearly a warning sign. You may need to look for more affordable housing or reduce your fixed expenses.

30% for wishes

These are expenses that improve your quality of life, but are not essential:

- Places to eat out

- Entertainment (Netflix, Spotify, movies)

- Clothes that are not strictly necessary

- Travel and vacations

- Hobbies and sports

- Delivery when you could be cooking

Key: On the other hand, this category is where you have the most room to adjust if you need to save more.

20% for savings in Rule 50 30 20

This money is for your future:

- Emergency fund (3-6 months of expenses)

- Extra debt payments

- Investments

- Savings for specific goals (travel, car, house)

Tip: Treat this 20% as another fixed expense. For example, you could “pay yourself first” as soon as you receive your salary.

How to apply the 50-30-20 rule step by step

Step 1: Calculate your net income

Use the money you actually have left after taxes and deductions. If you are an employee, this is what is deposited into your account. If you are a freelancer, deduct the single tax, income tax, or other taxes, as applicable.

Step 2: Multiply by the percentages

- Income x 0.50 = Limit for needs

- Income x 0.30 = Limit for desires

- Income x 0.20 = Savings goal

Step 3: Record all your expenses

For one month, write down absolutely everything you spend. Every coffee, every bill, every purchase. This is essential to understanding your real situation.

Tip: Use Biyuya to easily record your expenses on your phone. It’s 100% free and automatically categorizes your expenses.

Step 4: Categorize each expense

At the end of the month, review each expense and assign it to one of three categories: need, want, or savings.

Step 5: Compare and adjust

Do your needs exceed 50%? Do your desires consume everything? Were you unable to save 20%? Now you know where to make adjustments.

Real-life example: Ana and the 50-30-20 Rule

Ana earns R$ 600,000 per month. Before using the rule, she didn’t know why she could never save money.

Its ideal distribution (50/30/20):

- Requirements: $300,000

- Desires: $180,000

- Savings: $120,000

Your reality before applying the rule:

- Requirements: $320,000 (53%)

- Desires: $250,000 (42%)

- Savings: $30,000 (5%)

What has been adjusted:

- Changed cell phone plan (-R$ 8,000/month)

- Reduced the number of deliveries from 8 to 3 times per month (-$40,000/month)

- Cancelled subscriptions that were not being used (-$12,000/month)

Result: Now saves $90,000/month (15%) and continues to improve.

How to adapt the 50-30-20 rule to your situation

However, the rule is not rigid. You can adapt it according to your financial situation:

If you earn little: perhaps your distribution should be 60/30/10 until your income increases. The important thing is to save something.

If you have high-interest debts: consider a 50/20/30 split, allocating more resources to debt repayment.

If your rent is too expensive: maybe it’s 60/25/15. But use this as a sign to look for more economical options.

If you have no debts and earn well: you can be more aggressive: 50/20/30 with more savings.

How do I apply the 50-30-20 rule if I get paid daily or weekly?

If you do not receive a fixed monthly salary and your income is daily or weekly, the 50-30-20 rule can also be applied.

First, you need to calculate a monthly average. To do this, add up your income from the last 3 to 6 months and divide it by the number of months. This number will be your estimated base.

In addition, it is advisable to create a “stability reserve”: when you have a good week, do not spend everything. Save an extra portion to cover weaker weeks.

Finally, you can apply the rule on a weekly basis. That is, divide each income into 50% for needs, 30% for wants, and 20% for savings as soon as you receive it.

In contexts of high inflation or unstable incomes (as in Argentina), this adaptation is especially useful for maintaining financial stability without relying on a fixed salary.

Common mistakes when using the 50/30/20 rule

1. Confusing needs with desires

Starbucks coffee isn’t a necessity. Neither is driving your car when you could take public transportation. Be honest.

2. Not recording small expenses

Small expenses (coffee, snacks, apps) can easily add up to between R$ 30,000 and R$ 50,000 per month. Record everything.

3. Give up if it’s not perfect

In reality, you won’t be able to achieve exactly 50/30/20 in the first month. And that’s normal. The goal is to improve gradually.

4. Do not automate savings

If you wait until the end of the month to save “whatever is left,” then there will never be anything left. Set aside 20% as soon as you receive your salary.

How Biyuya helps you with the 50-30-20 rule

Biyuya makes applying the 50/30/20 rule simple:

- Record every expense in seconds from your cell phone

- Automatic categorization to determine whether it is a need or a desire

- View your actual distribution compared to the ideal one

- Track your progress month by month

The best part: it’s 100% free and you don’t need to download anything. Just go to app.biyuya.com from any device.

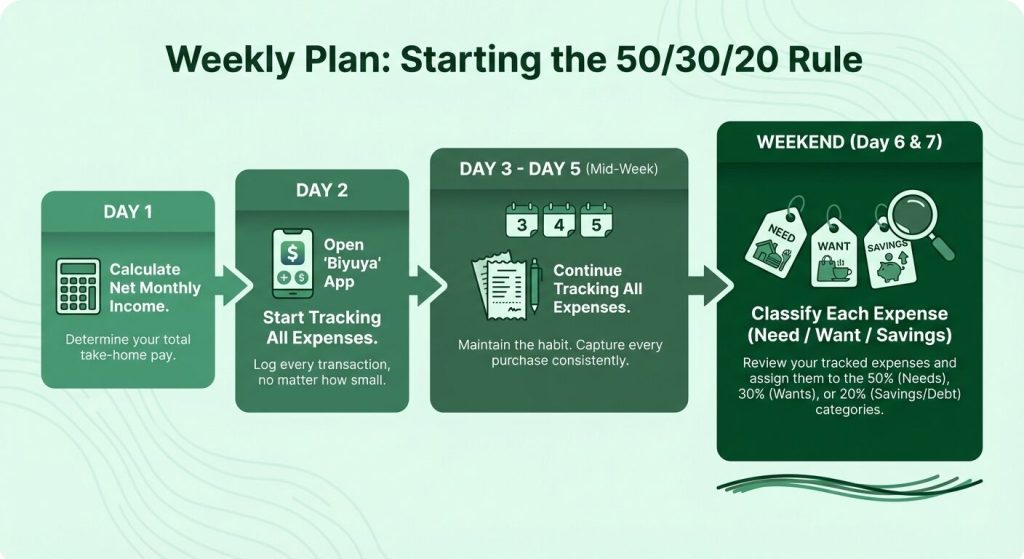

Action plan: your first week with the 50-30-20 rule

Day one: Calculate your net monthly income

Day two: I opened Biyuya and started recording my expenses.

Day three onwards: Record absolutely everything you spend.

Weekend: Classify each expense as a necessity/desire/savings.

Frequently asked questions about the 50-30-20 Rule

Yes. In that case, it’s recommended to calculate a monthly average based on the last 3 to 6 months.

That’s a warning sign. You may need to adjust housing, transportation, or look for ways to increase your income.

Yes, although it may require adjustments depending on inflation and the cost of living.

No. It’s a flexible guideline.

Yes, but it requires dynamic adjustments in the needs category.

Start with 5% or 10% and increase gradually. The most important thing is to start.

Conclusion

The 50-30-20 rule is not a magic formula; however, it works when applied consistently. It offers a simple and organized structure for you to take real control of your personal finances without going crazy with complicated spreadsheets.

The first step is to know where you are today. Only then can you improve.

If you want to apply the 50-30-20 rule in a practical way, tools such as Biyuya can help you plan your budgets better.

Sign up for Biyuya and start tracking your spending today. It’s 100% free.